The Obvious Alternative Investment

Thursday, July 28, 2016

The Obvious Alternative Investment

Rental homes can be a natural alternative investment choice for homeowners because they are already familiar with houses. Maintenance on a rental is not that much different than on your personal home. The same plumbers, painters and other workmen can be used to make repairs.

|

|

Single family homes offer an investor high loan-to-value mortgages at fixed interest rates for long terms on appreciating assets with defined tax advantages and more control than other investments.

- High loan-to-value mortgages – most investments require that you pay cash but rental properties can be purchased with 20% down payment.

- Fixed interest rates – most commercial loans are based on a floating rate such as prime interest plus one or two percent compared to real estate loans as fixed rates for the term.

- Long terms – commercial loans are generally short-term such as six months or a year with the possibility of being renewed for another six months or a year unlike real estate where a 30-year mortgage is commonplace.

- Appreciating assets – real estate has a long-term history of going up in value.

- Defined tax advantages – many investments are taxed as ordinary income but rental real estate enjoys a non-cash deduction called cost recovery, the profits from sale are taxed at lower long-term capital gains rates or may be eligible for a tax-deferred exchange.

- Control – rental homes don’t require partners and afford the investor more options than investing in mutual funds and other traditional investments.

The demand for good rentals is strong and the rents continue to go up in most markets. There are people who choose not to buy or cannot buy a home who would prefer to live in a single family home rather than an apartment.

Add Comment

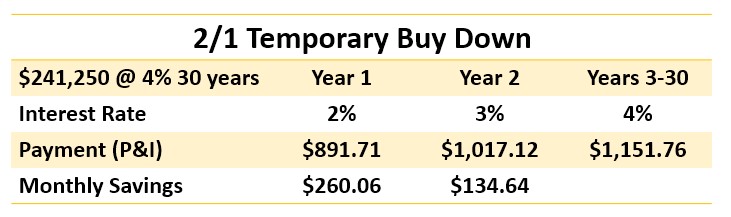

There is an infrequently-used mortgage program available that could be the solution to a buyer's or seller's problem.

There is an infrequently-used mortgage program available that could be the solution to a buyer's or seller's problem.

Buying rental property can be an excellent decision and the better informed you are, the more likely you'll have favorable results. The following suggestions can help you with your decisions.

Buying rental property can be an excellent decision and the better informed you are, the more likely you'll have favorable results. The following suggestions can help you with your decisions. "If I tell you it's going to rain, you can put the buckets on the porch." If you grew up in the south, you made have heard this expression when a person is testifying to the veracity of his word. If you know a person and/or their reputation, you know whether you can trust their word or not.

"If I tell you it's going to rain, you can put the buckets on the porch." If you grew up in the south, you made have heard this expression when a person is testifying to the veracity of his word. If you know a person and/or their reputation, you know whether you can trust their word or not. Most of us understand the expression "burning the candle at both ends" to mean working so hard that you burn yourself out. Normally, that wouldn’t be a good idea unless it is intentional.

Most of us understand the expression "burning the candle at both ends" to mean working so hard that you burn yourself out. Normally, that wouldn’t be a good idea unless it is intentional.