Temporary Buy Down

There is an infrequently-used mortgage program available that could be the solution to a buyer's or seller's problem.

There is an infrequently-used mortgage program available that could be the solution to a buyer's or seller's problem.

A temporary buydown is fixed rate mortgage that the seller has prepaid interest at closing to lower the payments for a number of years. The borrower must qualify at the note rate but gets the benefit of lower payments for the early years.

A 2/1 is a common buydown that the first year's payment is calculated at 2% lower than the note rate and the second year's payment is calculated at 1% lower than the note rate. The third through thirtieth years' payments are the note rate.

Let's set the scene. A buyer is using their available cash for down payment and closing costs to get into the home. They'd like to put their own touches on the home when they move in but may not be able to for a year or two since most of their cash was used.

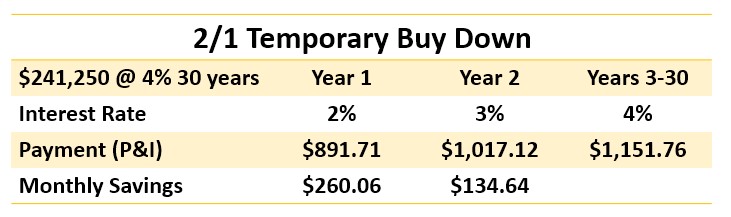

In this example, a $250,000 home is purchased with a 3.5% down payment and a 4% mortgage for 30-years. Normally, the principal and interest payment would be $1,151.76 for the full 30-year term. If the seller will pay the lender $4,736 at closing, it can be applied to pre-pay part of the interest for the first two years.

The first year, the buyer's P&I payment will be $891.71 for 12 months based on a 2% interest rate or 2% lower than the 4% note rate. It is $260.06 lower per month in the first year. The second year, the buyer's P&I payment will be $1,017.12 for the next 12 months based on a 3% interest rate or 1% lower than the 4% note rate. It is $134.64 lower per month in the second year.

A bonus for the buyer will be that the cost of the buydown paid at closing by the seller becomes prepaid interest that is deductible by the buyer in the year of purchase. The buyer gets lower than normal payments for the first two years and a sizable tax deduction.

This type of program can be very beneficial to a seller who wants to offer terms to improve the marketability of their home rather than lower the price. The challenge will be explaining it to not only potential buyers but even agents who are not familiar with this program.

Buying rental property can be an excellent decision and the better informed you are, the more likely you'll have favorable results. The following suggestions can help you with your decisions.

Buying rental property can be an excellent decision and the better informed you are, the more likely you'll have favorable results. The following suggestions can help you with your decisions. "If I tell you it's going to rain, you can put the buckets on the porch." If you grew up in the south, you made have heard this expression when a person is testifying to the veracity of his word. If you know a person and/or their reputation, you know whether you can trust their word or not.

"If I tell you it's going to rain, you can put the buckets on the porch." If you grew up in the south, you made have heard this expression when a person is testifying to the veracity of his word. If you know a person and/or their reputation, you know whether you can trust their word or not.